- Forex rollover charges in Euro pairs have surged since yesterday

- We saw a similar dynamic last month and into the end of the first quarter

- Traders should be wary of holding Euro short positions into the close

Why are Rollover Rates so High?

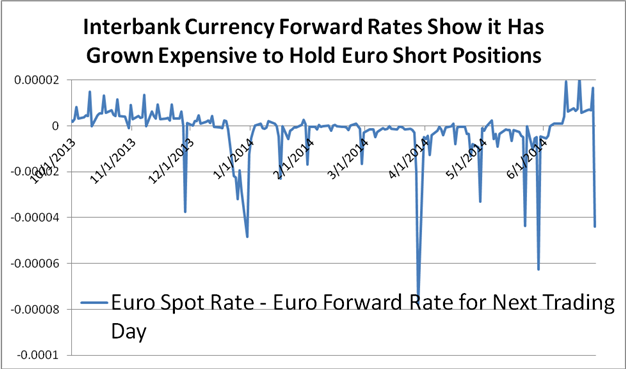

A look at interbank forward markets shows that holding Euro short positions versus the US Dollar and Japanese Yen has become exceedingly expensive since yesterday.

Those forward rates showed that traders could earn interest rate credits in holding EURUSD-short positions just yesterday. Yet a sharp shift now means that being short EURUSD is now at its most expensive since a similar spike in borrowing costs at the end of last month.

Source: Bloomberg Generic Price – “Consensus” Pricing

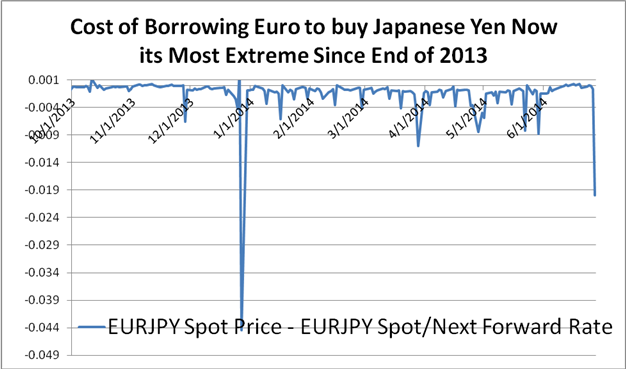

Indeed we saw an even more pronounced surgeinto the end of the first quarter, and it seems as though traders may continue to expect similar spikes at month and quarter end. The effect is likewise pronounced in Yen pairs, and the Euro/Yen in particular has seen large jump in overnight borrowing costs.

Source: Bloomberg Generic Price – “Consensus” Pricing

Interbank rates imply that today’s charge on the Euro/Yen in particular is the rough equivalent of the past 25 days worth of interest rate charges. Traders should be wary of holding a EURJPY-short position into today’s New York session close, as this is when rollover charges/credits are debited or credited.

Given that FX market volatility currently trades near record-lows, these charges represent an especially large cost to a trader looking to capture smaller currency moves. Indeed, the sharp changes in interbank lending markets could in some cases make the difference between a winning and losing trade.

Understanding Forex Rollover

Trading forex on leverage involves borrowing one currency in order to purchase another. In effect this means traders will pay interest rates for the currency which they sell, while they receive interest rate payments for the currency which they buy. In FX terminology this is most often called “Rollover” or “Swaps”.

Overnight interest rates will guide whether the trader will ultimately pay to hold a position or earn interest on the trade, and any sharp changes in the supply or demand for a specific currency can shift overnight interest rates in a hurry.

This dynamic can be very seamless to the trader, and indeed the parent company of DailyFX in FXCM Inc. posts the Rollover rates for both “Buy” and “Sell” orders directly on their trading platform.

Read more on forex rollover on FXCM.com

Written by David Rodriguez, Quantitative Strategist for DailyFX.com

Careful Holding Euro Short Positions as Borrowing Costs Surge

No comments:

Post a Comment